Something interesting and noteworthy occurred this past week.

No, not Mrs. Clinton’s surreal road trip to Iowa, the bizarre Chipotle stop, or the mystifying, scripted sit downs with “average Americans” – who turned out to be loyal partisans hired by the Clinton campaign to look earnest and interested for the cameras.

No, far away from the mobile Potemkin village that is the Clinton campaign, NJ governor Chris Christie got up in front of a group of actual voters in New Hampshire and told the truth.

Entitlements are on track to bury our nation financially, and with it, our long term prospects for prosperity for our children and grandchildren.

To his credit, in discussing this existential problem, Christie moved beyond generalities and bromides, committing an act of courage (or political suicide) by specifying the hard medicine necessary to rebalance our national finances and social responsibilities.

Under Christie’s plan, future seniors earning more than $80,000 would see their Social Security benefits begin to phase out, ending entirely for seniors earning more than $200,000. Christie would also raise the early retirement age from 62 to 64, and the regular retirement age from 67 to 69. The Governor also called for additional means-testing for Medicare and reforms for Social Security Disability Insurance to ensure that the truly disabled are the beneficiaries.

Reaction was quick, skeptical and fierce. The news headlines alone tell the story.

The Salon website featured an article, “Chris Christie’s dangerous Social Security demagoguery: Cloaking the plutocrats’ agenda in populist rhetoric.” Marketwatch.com was more straight forward, ”Christie’s bold plan to destroy Social Security by turning it into welfare.”

And fears that proposed changes to Social Security and other entitlements are the “3rd rail” of politics are broadly borne out. Public opinion surveys continually show that Americans of all parties do not want Washington tampering with Social Security. According to Harry Enten from “Five Thirty Eight,” website, in a January 2013 Reason-Rupe survey, 56 percent of Americans were broadly against changes to Social Security similar in scope to Christie’s proposals.

Interestingly, considering Christie’s political roots, Republicans are more likely than Democrats, independents and the general public to say that income should not be a determining factor in receiving Social Security benefits. Only 26 percent of Republicans believe that Social Security should go to only those below a certain income level. Seventy percent of Republicans are opposed to such a proposal.

However, the inflammatory rhetoric about the Christie’s plan belies the inescapable truth of the NJ Governor’s presumption; entitlements are set to swallow our nation whole if no changes are made. The longer we wait, the worse it gets.

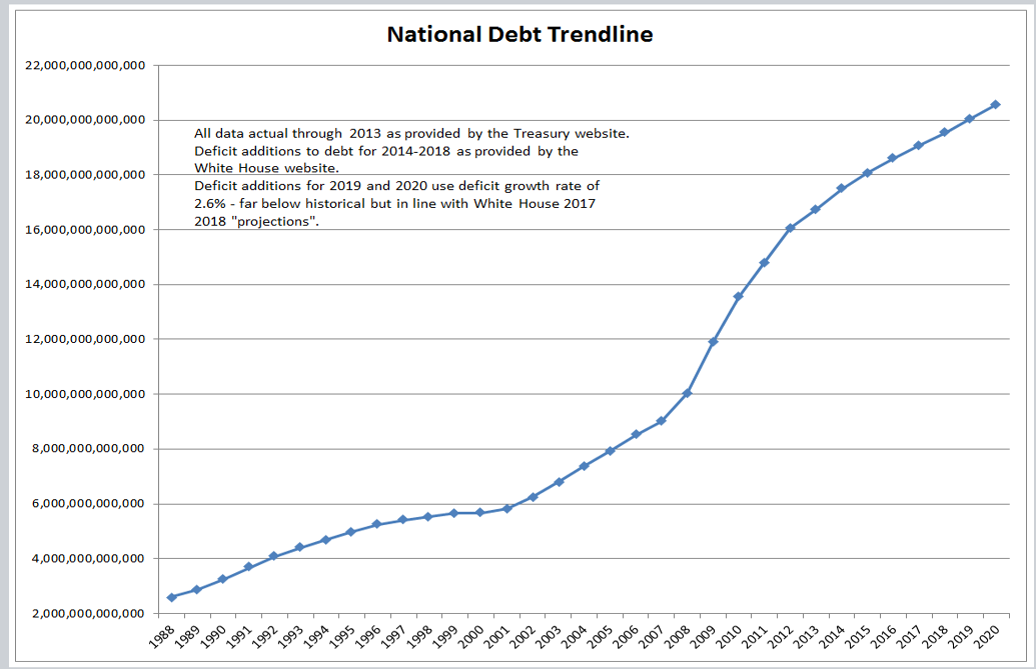

First, our national debt is on course to increase significantly:

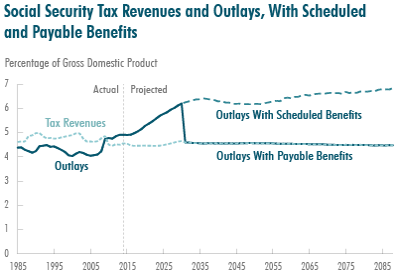

That growth in debt will be fueled, in large part, by entitlements:

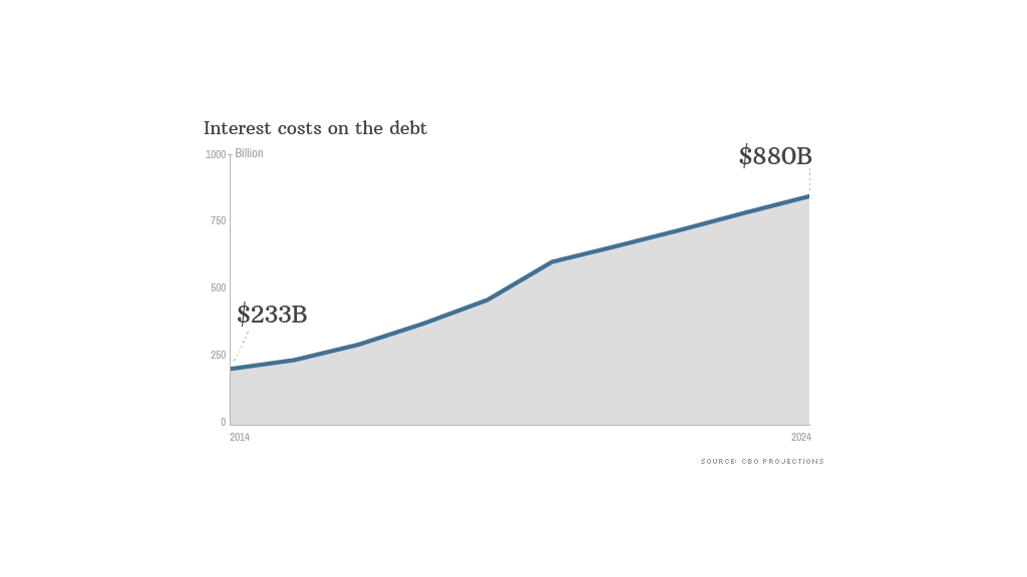

In less than a decade, that additional borrowing to fund entitlements will force interest payments on the national debt to skyrocket to nearly $1 trillion a year:

This result is completely unsustainable for the nation’s long-term fiscal health without dramatic action now. What is worse for this crucial national debate is how genuinely ill-informed we are as a people. The truth of Social Security is deeply at odds with the fiction that most Americans believe.

As I said in a post from December 2012:

“The Social Security Trust Fund, administered by the Social Security Administration, collects payroll taxes from workers and employers and makes benefit payments to retirees, survivors, and the disabled. But contrary to what many Americans believe – that the funds they pay are invested for their own retirement – Social Security actually is a “pay as you go” system, where payments collected today are immediately disbursed to pay benefits. There is no “savings account” per se.

In 1945, when there were 41 workers to support one retiree, and the average life expectancy of a Social Security recipient was 63, the program was actuarially sound. Today, there are only three workers to support one retiree (and that ratio continues to decline), while American life expectancy is now 79, requiring benefit payments for a much longer period of time. Typically, retirees are paid 1/3rd more in benefits than the total of their lifetime contributions.

Still, over the last 30 years, when the Baby Boomers were in their prime working years, Social Security was flush, taking in more in far more in payroll taxes than it was paying out in benefits.

But that surplus, about $2.7 trillion, was “borrowed” by the Treasury Department in an intra-government transfer over the decades, which was then used to fund other government programs on an annual basis. In return for the actual hard cash, Treasury deposited interest bearing bonds in the Trust Fund – an Uncle Sam IOU.

This intra-governmental transfer – the government effectively borrowing from itself – creates a surreal parallel universe in political budgeting matters.

For Democrats, the bonds deposited by Treasury in the Social Security Trust Fund are tangible, interest bearing assets that are redeemable. For official budgeting purposes, the Congressional Budget Office (CBO) agrees, projecting that with these assets, Social Security will be solvent for decades. When payroll tax collection and interest on the bonds no longer covers the bill (2015) for the greatly expanded number of retirees, the Trust Fund can begin redeeming its bonds to cover any shortfall.

But that’s the problem.

The bonds that Treasury has issued to the Trust Fund – as well as the interest those securities are generating – are not secured by anything more than the promise of the federal government to pay at a later date.

Thus, for the purposes of clarity, the US government did not borrow the Social Security surplus and invest it in something that generated greater returns than the interest Treasury was paying to the Trust Fund. It simply used the money to fund current expenses – nothing different than a consumer using a credit card to cover a shortfall at the end of the month – except that the feds did it with a generation’s worth of retirement money.

Stated plainly, there is no separate account holding Social Security investments for disbursement when the time is right. The fact is that almost 60 percent of the $4.7 trillion in intra-government borrowing represents Social Security IOUs that are going to come due. And here the math is the same as it is with the debt as a whole. The US will either have to significantly cut discretionary spending (including defense) or raise taxes in order to retire (pardon the pun) this liability. Fulfilling this obligation does not come without significant economic pain for most Americans.”

Which brings us to another under-asked question on Social Security; under this scenario of an unreformed Social Security program, who actually pays?

It won’t be the retirees or near retirees – they will be expecting their checks.

The burden of this looming financial catastrophe will fall on those who are today 16-40. The options will be massive tax hikes or eviscerating budget cuts, or both.

Think Greece, with all the economic instability that comes with it.

It is nothing short of generational theft, with income transfers on a scale unimagined before, with broad and negative social consequences for generations to come.

And for what? Senior poverty writ large has been declining relative to other demographics groups who have arguably lost ground:

| Year | Age | Poverty |

| 1975 | 0-18 | 12% |

| 19-64 | 7% | |

| 65+ | 13% | |

| 2013 | ||

| 0-18 | 20% | |

| 19-64 | 14% | |

| 65+ | 10% |

Indeed, the allocation of wealth in America by age clearly demonstrates that seniors are the most financially secure demographic:

| NET WORTH BY AGE OF HOUSEHOLDER | |

| Less than 35 years | 6,676 |

| 35 to 44 years | 35,000 |

| 45 to 54 years | 84,542 |

| 55 to 64 years | 143,964 |

| 65 years and over | 170,516 |

| 65 to 69 years | 194,226 |

| 70 to 74 years | 181,078 |

| 75 and over | 155,714 |

Today’s pending Social Security crisis is not only unsustainable, it also places the burden of financing near-term public pensions for seniors on the backs of those with the least ability to afford the crushing burden. Demographically, it is a trend only made worse by the weak economic recovery and its disproportionate impact on younger workers who have not made traditional career/wage gains.

For Millennials, who twice voted overwhelmingly for President Obama, and perhaps long for a populist firebrand who will “take it to the Man,” it’s important to note that progressive darling, Senator Elizabeth Warren wants to increase Social Security benefits.

In the final analysis, for all the fuss made about Christie’s plan, the real impact would most likely be a modest (though necessary) course correction. According to the Current Population Survey, only 5.1 percent of seniors 69 and older earn more than $80,000. Only .7 percent earn more than $200,000 (about 200,000 people). Retirees and near retirees are exempted.

But the modest beginning takes nothing away from Christie’s courage in starting the conversation. In a crowded field of Republicans, it would do the Party well to find other voices of reform on what is the central issue affecting our long term prosperity as a nation.